Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

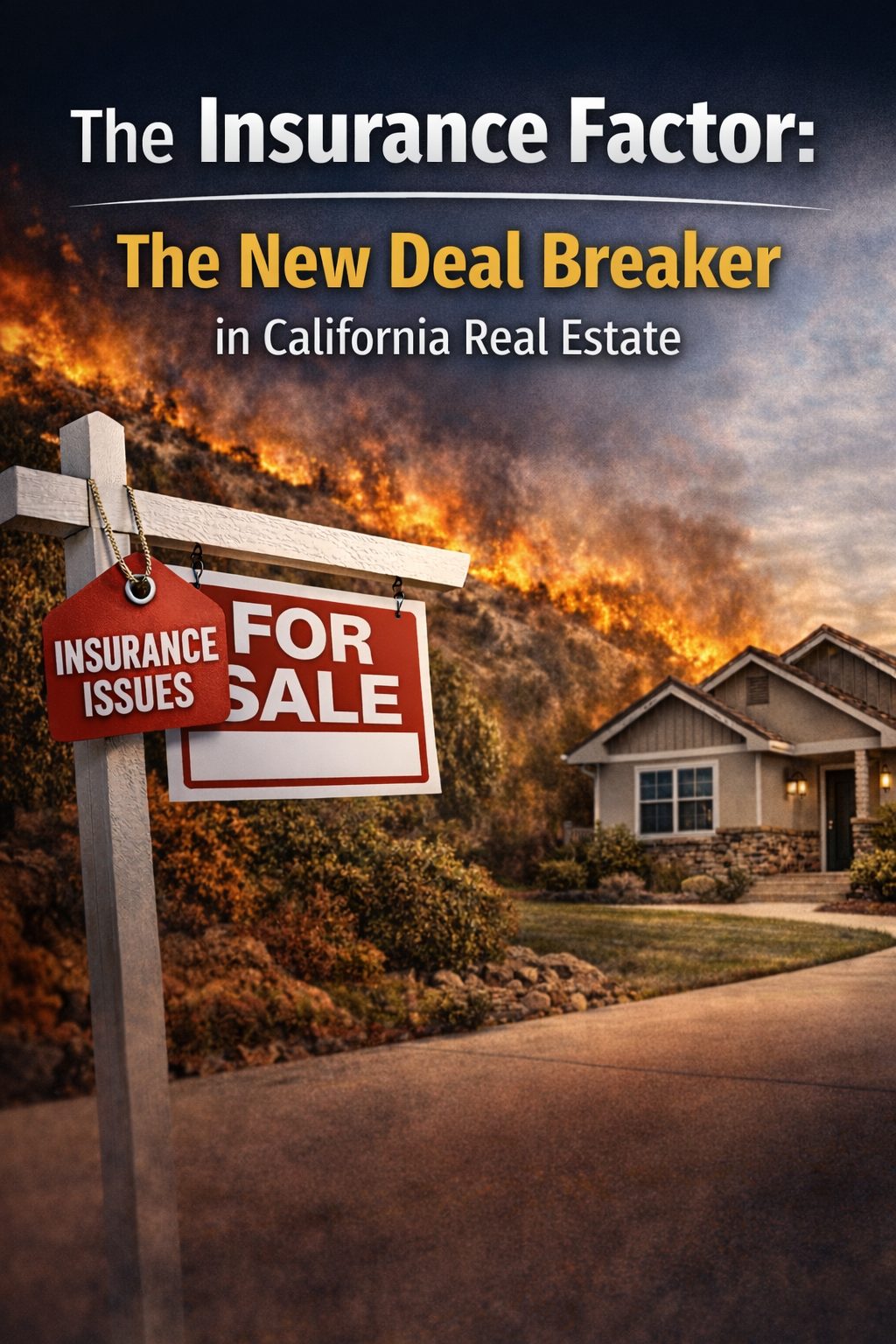

For decades, buyers focused on price, interest rates, and location.

In 2026? There’s a new variable quietly killing deals:

Homeowners insurance.

Across Los Angeles and Ventura County — from West Hills to Calabasas, Woodland Hills to Thousand Oaks — insurance is no longer a routine checkbox. It’s becoming a make-or-break factor in real estate transactions.

Let’s break down what’s really happening.

Why Insurance Is Suddenly a Problem

Insurance carriers have:

- Pulled out of certain California markets

- Tightened underwriting guidelines

- Increased premiums significantly

- Required property upgrades before issuing policies

Buyers are discovering — sometimes late in escrow — that:

- Coverage is limited

- Policies are expensive

- Or they’re being pushed to the California FAIR Plan

When that happens, financing can be delayed… or denied entirely.

And that’s when deals fall apart.

How Insurance Impacts Loan Approval

Here’s what many buyers don’t realize:

Lenders require proof of insurability before funding a loan.

If a property:

- Has an older roof

- Has outdated electrical panels

- Is in a high fire-severity zone

- Lacks defensible space

It can trigger insurance complications.

No insurance = no loan.

It’s that simple.

What Sellers Need to Understand Before Listing

This is where strategy matters.

Before going live, sellers should:

- Review current insurance policy details

Know the premium, carrier, and renewal status. - Evaluate property condition

Roof age, plumbing, electrical, brush clearance. - Consider a pre-listing insurance quote

If buyers struggle to get coverage, your home becomes harder to sell.

The homes that are moving right now?

They’re clean, well-maintained, and insurance-ready.

Buyers: Don’t Wait Until Escrow

If you’re shopping in areas like Agoura Hills, Hidden Hills, Chatsworth, or Oak Park — especially near hillside or brush zones — you should:

- Speak to an insurance broker before writing offers

- Budget realistically for premiums

- Verify roof age and upgrades early

The old mindset of “we’ll deal with insurance later” doesn’t work anymore.

The Bigger Market Shift

Insurance isn’t just a paperwork issue.

It’s affecting:

- Property values

- Buyer demand

- Negotiation leverage

- Time on market

Homes with updated systems and insurability clarity are gaining a competitive edge.

Homes without it?

They’re sitting.

The Bottom Line

In today’s Southern California market, pricing matters. Presentation matters.

But insurability may matter just as much.

If you’re buying or selling in the LA and Ventura County corridor, insurance strategy needs to be part of the conversation from day one — not day twenty-one.

The market has evolved.

Smart sellers and buyers evolve with it.